BlogWelcome to the Donegans' blog. Start reading for help with investing, financial independence, lifestyle design, and many mini-experiments!

|

|

|

Back to Blog

What is an index fund? Investor Series10/11/2020

What is an index fund? The language of investing can be hugely complex at the best of times! Even a simple term like index fund takes a lot to properly explain. If you want to feel confident investing then the first step is to build your investing knowledge and financial vocabulary. The more you understand something the more confident you will feel starting! Writing this article has doubled Katie's and my knowledge about index funds! We hope it does the same for you!

The short explanation: Index funds give you an easy and cost-effective route to diversify your investments across the globe and partake in the growth of the global economy. Sounds sexy; but what the hell does it mean! What is an index fund? What is contained in an index fund? Which index funds should I buy? Why do I care? Let's get geeky together!

Updated: 22nd June 2021

Disclaimer: This is not financial advice. Katie and I are not trained financial advisors, nor to we pretend to be one online. Read our full disclaimer here.

Who created index funds?

The first index fund available to retail customers was launched by Jack Bogle way back on 31st December 1975. He built it to allow anyone to be able to invest in the stock market easily and at a low cost. Around the same time Jack founded the company Vanguard with a simple and clear mission:

"our mission is to take a stand for all investors, to treat them fairly, and to give them the best chance for investment success"

He wanted to make it possible for anyone to be able to invest in the stock market with low fees. He did this by creating an index that tracks a market which means that the fund invests in all companies in the market in proportion to the size of the company.

His first one tracked the S&P500 and is called the Vanguard 500. It is still in operation to this very day. The S&P500 is a list of the 500 largest companies listed on the stock exchange in the USA When he launched this product and made it available to everyone, he was derided by Wall Street and the old guard of Financial Companies. They could see their profits disappearing if the idea of low cost, index funds caught on and they went on the attack. "Enough history Alan" I hear you cry! I find it fascinating and you will be able to see why I believe so strongly in Jack's company and mission. He tore down the elitism of investment and democratised it, in other words made it available to everyone. This is what I have been wanting to do for entrepreneurship with the Rebel Business School and Rebel Entrepreneur podcast. Anyone should be able to build a business, make their own money and invest and save. Reader comment: Maia from Berkshire asks "I am curious – are you sponsored by Vanguard, or do you get a commission? I just wondered why you only discuss them…" Good question. I don't get commission. I wish! lol. I am not sponsored. I believe in the original mission of the founder Jack Bogle and what the company stands for. Plus it is easy for me to recommend them as all of Katie and my wealth is invested in their funds. I find it hard to recommend other funds as I don't use them. What does low cost/low fees mean?

When you invest in an index fund you have to pay for the privilege. As well as the cost of actually buying the fund there are various fees involved. One of them is the annual management charge (AMC) and covers the cost of managing the fund. When I say low cost or low fee I mean that the AMC is very low. For Vanguard index funds the AMC varies from 0.06% to 0.29% depending on the fund.

These fees are a lot lower than the AMC for actively managed funds. In actively managed funds someone chooses the companies that the fund buys rather than just buying all the companies in the market and you have to pay more for this. The AMC can be as high as 1% or 2%. This doesn't sound like a lot but when you compound this over time it can cost your investments thousands and thousands. Want to know more about theimpact of fees over time? 1% doesn't sound like a lot but it can cripple your financial future. Alan and Katie’s investment strategy

After my dad persuaded me to invest my life savings in an actively managed high-tech, high growth fund which ended very badly, I was scared of investing in the stock market for more than a decade!

The change came when I read Money Master the Game by Tony Robbins and started learning about investing. Whatever you do; avoid that book. There are far easier ones to understand! Katie and I built up the confidence to have another go at investing. But it wasn't until we met JL Collins author of The Simple Path to Wealth (Do read this one!) in Ecuador at the FI Chautauqua that we really understood the power of index investing and went full in!

JL Collins, Katie and Alan at the UK Chautauqua in 2017

JL helped us to see that by investing in index funds we could benefit from the growth of companies around the world by becoming owners. We didn't have to choose companies individually (HUGELY risky!) we could choose to own a slice of the entire market and every company within it!

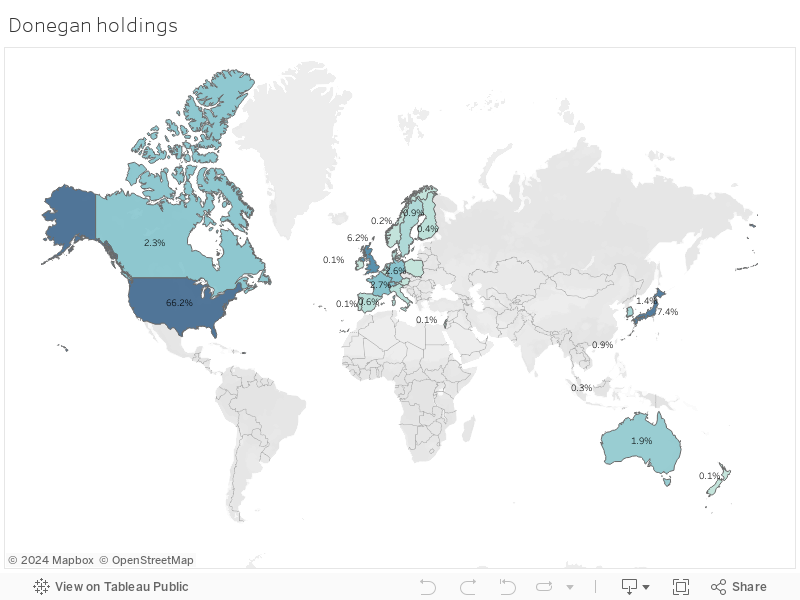

By buying an index fund you are buying an underlying asset. This underlying asset is actual companies like Apple, Netflix and Microsoft. You own a actual slice of those organisations and if they perform and make profit you get to share in that profit! Once we understood the power of index investing we took the money that we had saved up ready to invest and invested it in one giant lump sum into the Vanguard Developed World ex UK Index fund (we did this because we already owned a piece of the UK index separately.) This index fund allows us to own shares of companies all around the globe at a very low cost! To give context, on our first go at investing the fees were 2.21% compared to investing in the Developed World ex UK index fund which costs 0.14% The fees for the Vanguard fund are almost 16 times lower!!! We all make mistakes when we are starting out! Katie and I hope that us writing these articles will enable you to avoid the mistakes that we made. Katie has been geeking out over the data and creating us a range of amazing charts so that you can visually see what is in an index fund and differences between them! THANK YOU Katie!! Katie's charts are interactive so you can roll your cursor over them to see details, zoom in and out on the maps and more. They are best viewed on a bigger screen on a tablet or laptop so if you are reading this on your phone bookmark the page for when you get home! Here is a map of where all of our money is invested around the world and by what percentage. The darker the colour the more of our money is invested there.

Could you imagine if we had to organise all this ourselves? Could you imagine placing the order for 0.2% of my money to be invested in Norway stocks and shares, 0.1% in Israeli stocks and 0.3% in Singapore?

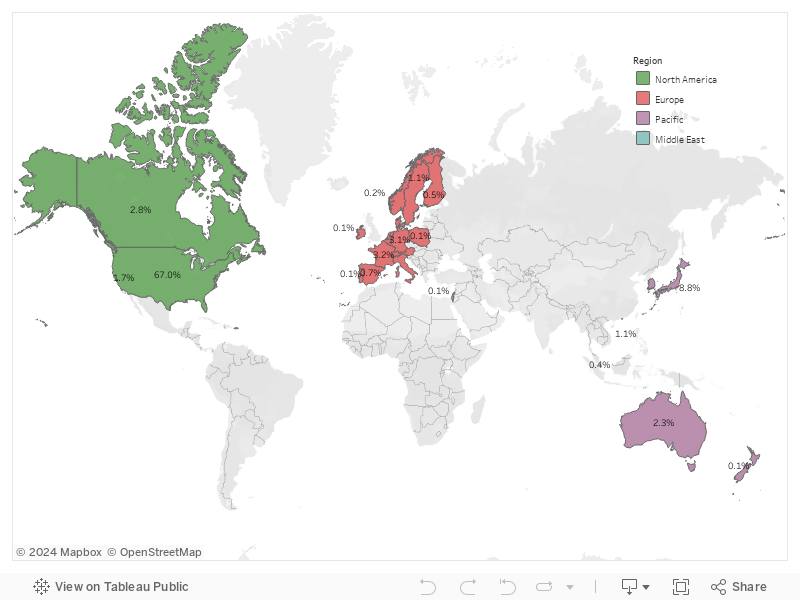

Index funds give us an easy way to buy stocks or shares of companies around the world at the click of a button! After you have set up and funded your account you can hit "buy" and invest an amount of money that will be automatically distributed globally! I find it amazing every time I invest in an index fund, I am buying a stake in 1000s of companies around the world! Every year Katie and I fill up our ISA allowance and invest £20,000 each into the Vanguard Developed World ex UK Index fund. This money is automatically taken and Vanguard buys shares in all these businesses around the world! I find it astonishing! The below chart shows where your money goes, by country and percentage, when you invest in the Developed world fund.

All the charts in this post and information were taken from from the Vanguard website (Sept'2020). The Vanguard website is updated monthly; for the latest figures check there! Katie and I have better things to do than check every single month!

What's in an index fund?

We get very excited about this stuff! So excited. SO EXCITED IT HURTS!

Alan & Katie after looking at the Vanguard Investor site!

Investing in these index funds has allowed us to get to a stage where we never have to work again! That's the whole point of this. I was 40 years old and Katie was 35 when we hit financial independence. I retired 25 years earlier than the average British person!

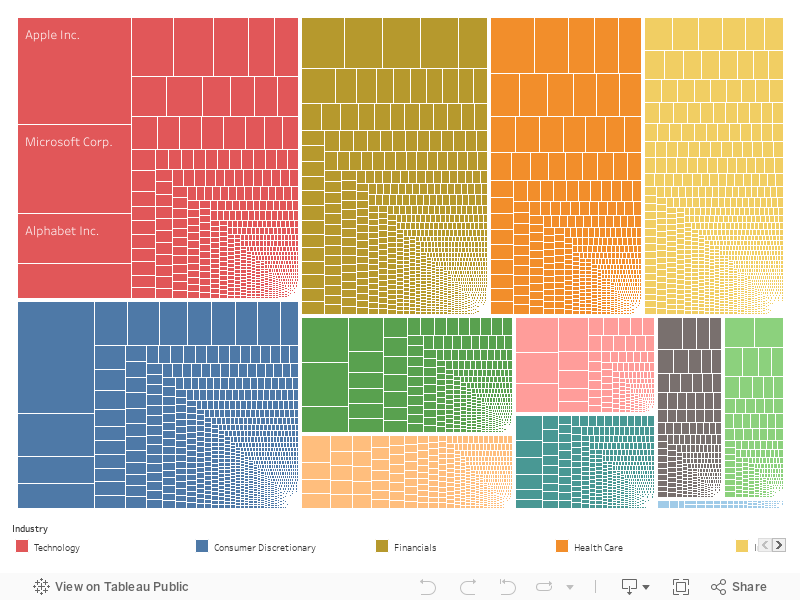

Well I am not entirely retired because we are working on this resource for you, but you get the idea........ So what is an index fund? It is a giant list of companies that normally mirrors a stock market. (A stock market is made up of companies which are bought and sold publicly. This is as opposed to companies that are privately owned like Lego! Oh man I wish Lego was in one of the index funds I buy....) When you buy an index fund you end up owning a tiny slither of each company on the entire list or index! They are generally designed to mimic the performance and composition of a financial market. For example the Vanguard 500 fund tries to mimic the Standard and Poor (S&P) 500. The Vanguard Developed world Ex UK fund tracks the performance of the FTSE Developed World EX UK Index. These funds make it easy for you to own a slice of every company in the market at the click of a button and benefit from average market returns! "Wait a minute Alan; average returns? I don't want average returns!" I can hear you screaming. The interesting thing is that average returns are just not that average. In an index fund you get to enjoy the average returns of the market (which is made up of all these companies). The only way to beat the market is to pick and choose companies to invest in or dance in and out of the market hoping to buy low and sell high! These are highly risky strategies and most professionals (let alone you or I) fail to beat the market. Average returns, as it turns out, tend to be far, far better than your average person will ever get! Katie and I are over the MOON with our average returns. We earn enough to live on each year without ever having to work again! Can't get much better than that?!? This next chart by Katie shows you what makes up an index fund by sector. She has taken the entire list of companies in the FTSE Global All Cap Index fund and visualised them by sector (shown by different colours) and amount of the fund that is made up by each company and sector (size of the coloured sections and size of the individual squares) As you scroll over each box it will show you the company name, sector it is in and percentage of your money that would be invested in that stock if you owned that fund. Open the chart and have a play around. It is so cool! The top left red sector shows technology and the biggest three companies in that sector are Apple, Microsoft and Google (Alphabet is the name of Google's holding company) Spend a few moments scrolling around the chart and you will see where your money goes, which industry and companies, when you invest in this fund!

What have we learnt so far?

The downside of index funds

What is the downside? Why isn't everyone doing this? What could go wrong?

Why isn't everyone investing in index funds? In 1975 when Jack Bogle launched the fund he managed to persuade people to start investing in his index. At the start he had pooled together $11m of investors' money. Fast forward to August 2020 and for the first time ever more money is invested in index funds than actively managed funds! There is $4.27 trillion invested in index funds worldwide compared with $4.25 trillion in actively managed funds. People are finally starting to see that the dream of above average market returns sold to us by investment companies and the financial industry is a folly and are moving their money to index funds. A lot of people already invest in index funds. What's the downside of index funds? The short answer is I haven't found one yet! But I went over toInvestopedia to have a look to see what they describe as the downsides of index funds. They say there are four main ones:

Below is my opinion about these downsides. It is important to realise that these are my opinions and before investing you MUST do your own research and work out what is best for you! Vulnerable to market swings and crashes All stocks and shares are vulnerable to this, not just index funds! If the market crashed then that is because the underlying companies have gone down in value as well. This is not an argument to go stock picking! Swings in the market and crashes affect all aspects of the market in different ways. The key thought that allows me to be comfortable with this downside is that over the long run the market always goes up. Yes it might be a volatile up and down ride but over the long run the market always goes up! By long run I mean 15 years plus. You have to be in it for the long term. You just need to brave out the storms, hold your investments and allow the market time to recover! Lack of flexibility I am not sure this is a real downside. You can get index funds that track bond markets, the US market, the UK market, Emerging Markets and the entire Globe! You can get index funds for property investments called Real Estate Investment Trusts (REITs) and indexes than cover just about everything else! And if you want to own a bit of extra Apple on the side then you can! Katie and I don't recommend it; but it is possible! No Human Element Thank you, thank you, thank you is my response. Most actively managed funds that are controlled by humans dance in and out of the market, they buy and sell to justify their existence and then historically under perform the market. Why would I EVER want human intervention as that brings emotion and illogical decision-making that leads to worse returns and higher tax bills!?? I, for one, am grateful that a human isn't moving my money around, lowering my returns and then charging me over the odds to pay for it! This to me is one of the biggest upsides to index investing! Limited Gains This is the one that the financial services industry and Wall Street wants you to believe. Your gains are limited in index funds and will just be average! They are right! You will just get average returns. What they don't tell you is that on average they (actively managed funds) get worse returns! Actively managed funds fail to outperform index funds over and over again. Yes your gains are limited to average but that is still better than most other people out there get. What they also don't tell you is that you own every company in that index. So for example if Apple has an amazing year and releases a new iPad and makes a fortune then you will share in that profit. If Netflix does really well or the next Airbnb storms the market you will enjoy the benefits of that as well. Your money is invested across all these companies and as such you enjoy the gains that they all get! What's next?

An index fund is a low cost way to invest your money in all the companies in a given market. It is a way for uneducated investors (this is me, Alan, I just don't have the time, energy or desire to educate myself about all the companies in the market and learn enough to stock pick) to be able to invest with lower long term risk.

Katie and I invest our money in Vanguard index funds and up until this point have invested almost entirely in the Vanguard Developed World ex UK.

Katie and I created a course to help people take control of their finances called Rebel Finance School. After running this twice we found we just could get all the information about investing into the course. The biggest hole in the course was helping people to choose an index fund to invest in and actually start!

These articles are our work to address that and to help you gain enough knowledge to choose an index fund to invest in. Investing is the key to providing for yourself in retirement and creating a stable financial future for you and your family. Index funds are the tool that Katie and I used to be able to retire 25 years earlier than average in the UK and we want to help you understand the power of these tools!

|

RSS Feed

RSS Feed