BlogWelcome to the Donegans' blog. Start reading for help with investing, financial independence, lifestyle design, and many mini-experiments!

|

|

|

Back to Blog

I didn't notice the weight slowly piling on week by week. A year passed and I was obese! I hadn't noticed the small change each week until it was too late. Fees are very similar. They are small enough that you don't really notice them at the time, they are hidden from you and they just gradually erode your wealth over time. You wake up a decade or two later and you aren't worth what you thought you would be! Fees are the hidden element in investing that makes everyone else wealthy apart from you! Let's tackle fees together Katie's investmentsOne of our first investments into the stock market was Katie opening up a stocks and shares ISA and buying a managed fund. Katie tells this one better than I do; so over to Katie. In case you haven't met her yet here is a picture of the two of us.  Katie: I had been working for Deloitte for a couple of years. I had started to earn good money and was feeling pretty pleased with my progress. One day my desk phone rang. This was quite unusual! No one ever rang me. I felt very important. I had learnt not to say “hello” when answering the phone. That was for civilians. Now I answered with “Katie Donegan”. Very professional. The man on the other end of the phone, James Smith (name changed to protect the “innocent”??), asked if I had thought about investing my hard earned cash. Well the answer was “yes” but I didn’t know how. We organised to meet at his offices in the City. A few days later I headed over to his offices which were VERY swanky. Glass partitions, a fancy coffee maker. I was impressed. I even knew what questions to ask, sort of. I asked him about passive investing vs active investing. I asked him about investing in property instead. I didn’t understand enough to be able to be firmer in my views. I started off investing £100 a month with him. I questioned the fees and how much higher it was than passive investing and his answers seemed to make sense. Years laterAlan is back now. I know you probably want more Katie; who wouldn't but our team works with me telling the stories and Katie doing the data and visualisations! She hasn't realised that she is a better writer than me already! Back to the example: we invested for a year or two with this company before we learnt about index investing (If you don't know what an index fund is read this). When we truly understood index investing we sold our investment in the managed fund (they tried to persuade us to stay) and invested it all in Vanguard index funds. Fast forward many more years and recently our VERY smart friend Matt was staying over at our flat in Basingstoke. He is as much of a geek as Katie and I and we got excited about analysing our investments with James Smith and Vanguard to see which one actually performed better and what the impact of those high fees were. Katie had found the paperwork for her old investments and we started to read and build a spreadsheet analysing the difference. I am not sure how to properly explain how difficult this was. It took three of us 3 hours to work this out. Reading the small print of the investments was really challenging to find out what fees we were actually paying. They were hidden in different paragraphs and on different pages throughout the documentation. Matt has a degree from Cambridge, Katie has a degree in Statistics and is an actuary and I eat pizza. Together we have some skills. Why am I telling you this? It took the three of us the equivalent of an entire work day to work out what we were paying in fees! Katie and I have just spent another day analysing the figures again to try and understand them. Imagine how confusing is it for someone with no investing knowledge! Some of these active investing companies make it difficult to understand on purpose so that you can never really work out what they are charging you. I am still not entirely sure how much they took but I can tell you the difference it would have made! What we discovered shocked us. The feesWhere does the money go! This is the bit that is really shocking about this whole system. The fees are kind of hidden from you. The Annual Management Charge (AMC) is just taken from your investments and you never see it disappear. All you see is how much you've gained not how much has gone missing from your account. If they made this transparent I think people would be SHOCKED at how much money they are bleeding.  You have to be careful when investing. How much of the money ends up in your pockets versus the financial institutions? So let's look at the different fees that finance companies may or may not be applying to your investments without you knowing:

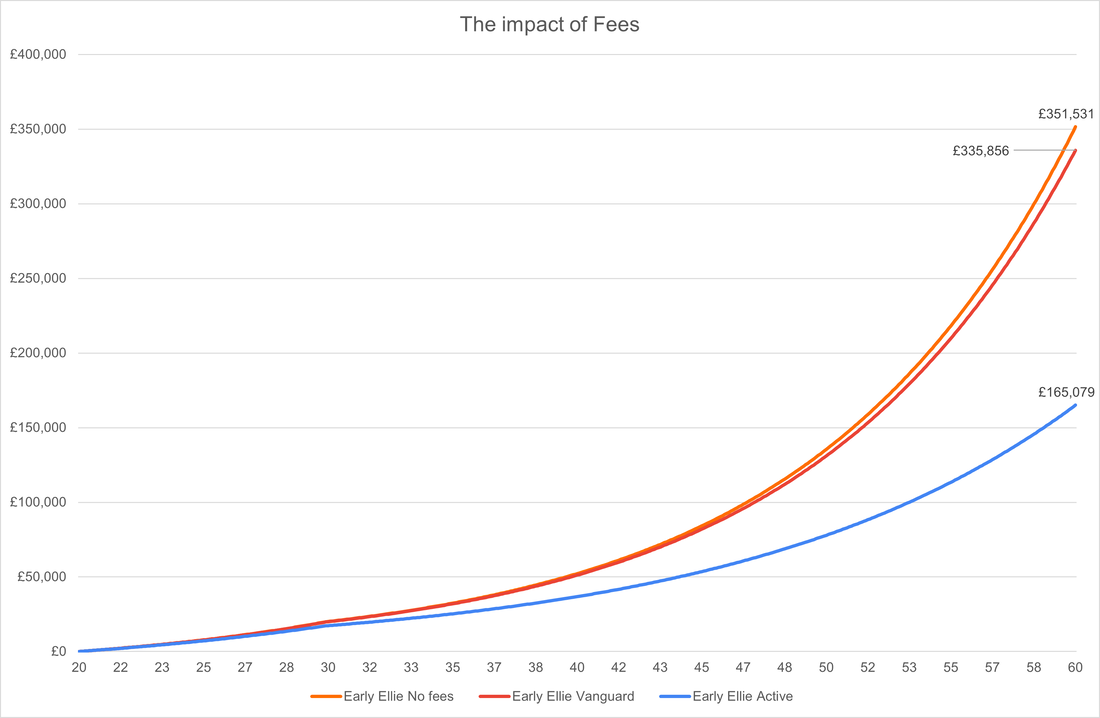

It is incredible how the money bleeds away without you noticing. Then the fund manager gleefully shows you that your account has gone up 5% without really showing you how much they have syphoned off and taken from you. The true cost of poor advice and feesKatie and I kept the investments above for a few years until we sold them off and invested in property instead. Eventually we found the FIRE strategies and learnt about Index Funds and passive investments. What would have happened to our investments if we hadn't discovered FIRE and we had followed James Smith's advice and strategy? Would we have made FIRE? For this comparison we have taken our current investments and where they have got to and compared that with the two funds that James Smith recommended minus their exorbitant fees! Let's tackle the 3% entry fee that they charged us for every purchase of their fund. I feel angry typing this! If we had continued with this over the course of our investing we would have given them £22,061. But this is small fry to the difference in the returns we would have got. It is virtually impossible to unpack the impact the 1.61% AMC fee as it is taken on a daily basis and just worked into the price of the fund. We spent an entire day trying to figure this out and couldn't. What we can tell you though is what the final position would have been. Our current strategy is investing in Vanguard Index funds. The current value of our stocks and shares is £1,028,966. If we had invested with James Smith and paid his high fees our net-worth would currently have been £713,296. That is a difference of £315,670 Through worse performance and high fees we would be THREE HUNDRED AND FIFTEEN THOUSAND POUNDS worse off! Fees destroy compounding and progress and we would not be FI right now if we had chosen to pay the higher fees and trusted the advisor. But it's only 1%It doesn't feel like a lot does it? 1%? It is a tiny amount. The 1% theory can work for you when you are improving. If you just work to be 1% better at what you do each day by the end of the year you will be 37 times better! Small improvements make a MASSIVE difference over the long run. The inverse is also true. Small amounts deducted from your accounts seem miniscule at the time but over time they are like an anchor for the performance of your investments. How big would you like the anchor attached to your investments to be? Imagine your investments are you on a bicycle climbing the hill towards your financial independence. The cycling and energy you put in is your savings. Now imagine you had an anchor attached to your bike that you had to drag up the hill. You get to decide how big the anchor is. The one from James Smith was HUGE. It was his salaries and his profits that we had to drag up the hill too. In fact the anchor that we had would have pretty much halted our progress up the hill, our investments would have hardly grown. The bigger the fee the bigger the anchor you are dragging along......... Let's look at EllieKatie has made up an imaginary investor Ellie. Ellis is a sensible investor and she starts early. She invests £100 a month starting when she is 20 and finishing when she is 30. Over 10 years she has invested £12,000 total. This chart shows the impact of fees and different funds on her investments  The Blue line at the bottom shows where her investments would have ended up if she had invested with the same fees that Katie did with James Smith. The Red line show where she would have got to if she had invested with Vanguard and paid their fees and the Orange line shows what she would have got if she had paid no fees at all! We assumed a flat growth rate of 10% return to isolate impact of the fees and only the fees. So we assumed the actively managed fund would get the same return as the passive; which is not true but we wanted to demonstrate the negative impact of high fees. On fees alone and the reduction in compound growth Ellie would have missed out on £170,777. This is insane. Fees can cripple your ability to retire if you choose the wrong thing! What's next?!Katie and I have been working on this series of articles to help you get to grips with investing and to help make it more straight forward. The full series covers:

If you want more help then we are planning on running another Rebel Finance School Course in 2021 and if you give us your email address on that page we will let you know when that is. In the mean time enjoy the articles and let us know how else we can help you in your goals and ideas. Remember, you build your life. Start creating and building a life you can be proud of day by day. Your daily habits and actions build your life. The extraordinary belongs to those that create it. Look out for a complete re-design of the website coming soon plus lots more. To make sure you hear all about the courses Katie and I give away and more sign up to the mailing list below Thanks for reading and being part of the team Alan & Katie Disclaimer: This is not financial advice. Katie and I are not trained financial advisors, nor to we pretend to be one online. Read our full disclaimer here.

|

RSS Feed

RSS Feed