BlogWelcome to the Donegans' blog. Start reading for help with investing, financial independence, lifestyle design, and many mini-experiments!

|

|

|

Back to Blog

I wandered around the counters in a trance, staring at an incredible selection of food. I didn't know what to choose or even where to start! After what seemed like 20 minutes of wandering I decided I needed to limit my options. I decided to have soup and headed to the soup section. There were 20 different soup flavours to choose from. I nearly had a melt down. I was just hungry and tired! I needed food!

This is the paradox of choice. The more options there are the harder it is to make a decision. This was just deciding what to have for lunch! Can you imagine how I felt looking at investment options for the first time? Maybe you can? The paradox of choice

If they had offered me "tomato soup or potato soup?" I would have been able to decide quite quickly and would have just named the one that was more exciting. Given two options it is easy to evaluate and pick one.

When there are multiple options all sorts of thoughts and chemical reactions happen in our brain. The fear of missing out rears its ugly head and we start to think about making the wrong choice. Somewhere deep inside our brains we know that by selecting one thing we are saying "no" to all other options at that point and we are worried; "What if I get it wrong?" The more options there are the harder it is for us to feel comfortable making a choice. There are hundreds if not thousands of index fund providers. One of them, Dow Jones Indexes has over 13,000 indexes on it's own!!

The Paradox of Choice. The more options there are the harder it is to actually make a decision and start

How are you meant to ever make a choice given the complexity and size of that offering? How can you ever analyse that amount of options to "know" you are making the "right" choice? No wonder people (including Katie and me in the past) get paralysed by the level of choice and never end up investing for their future!

Disclaimer: This is not financial advice. Katie and I are not trained financial advisors, nor do we pretend to be one online. Read our full disclaimer here.

Where to start? Decision Making

To get you investing there are several different questions you need to answer. Katie and I are going to do our best to walk you through the different options and help you get going. The primary questions are:

This is the reason why people don't actually push through and start investing. It is SO COMPLEX! Let's break it down and work together to make this easy! Make yourself a tea, get a custard cream and let's work through this! Choice 1: Which index fund provider should I go with?

Let's start with the simple answer. Katie and I have all our money invested with Vanguard. Why did we choose Vanguard? It is the fund provider that most of the Financial Independence / Retire Early (FIRE) community recommend; it is low cost and their interests are aligned with ours.

Just to be clear I am not being paid by Vanguard, sponsored or anything else to make this statement. Even though I am open to Lego gifts my integrity can't be bought. Katie and I started our journey into the Financial Independence Community by reading Mr Money Mustache (MMM) and then went to an FI Chautauqua retreat in Ecuador where we met JL Collins and heard him talk. JL is a HUGE advocate of Vanguard and its creator, Jack Bogle, and that inspired me to learn more. What did I discover that convinced me to invest? The first thing that really resonated with me was the fact that Vanguard is the only investment company that's goals are directly aligned with yours as the investor. In a normal financial institution the company makes money by making profits from its customers and then distributing those profits to its shareholders. The financial institution's success is determined by how much profit they make out of you, the customer. The primary objective of most financial instructions is not to help you to get wealthy but to make profits out of you! Vanguard is different as it is owned by the investors. If you own one of their index funds you own a share of the company. Therefore the only people it would be trying to make money out of and return profits to are you! The way they do this is to reduce the costs of the funds if they are in danger of making profits. Here is how Vanguard themselves describe it on their website:

The second reason Vanguard is recommended by a lot of people in the FI community is the low cost. Their index funds cost anywhere from 0.04% to 0.24% which is incredibly low! Compare this to the first active fund that Katie and I invested in which was 2.21%! That is nearly 16 times HIGHER!

Fees have such a HUGE impact on the lifetime performance of your investments. As part of this investor series of posts Katie and I are creating a post on fees and their impact. The final reason I invest with Vanguard is because some of the smartest people I know and respect such as JL Collins, MMM and Millennial Revolution also invest with Vanguard. Fidelity is another provider that gets recommended from time to time as well. Feel free to check them or other providers out. It is important to research your choices so that you feel comfortable! Choice 2: Which type of index fund should I choose?

There are so many different types of index funds you can invest in. Even if you have chosen to invest with Vanguard you click through to their site and there are 5 Life Strategy Funds, 11 Target Retirement Date Funds, 37 Index and Active Funds and 25 Exchange Traded Funds! Where do you start?

Let's get to it! What the hell do all these things mean and how do you make a choice? The quick and simple answer is go for Index funds. I was tempted to say that f you are happy with that answer skip ahead to the next section BUT I'm not going to say that! You should read this section so you understand why you are doing what you are doing and to develop your financial literacy. Let's go:

This image shows the LifeStrategy fund from the Vanguard website with a 40% bond, 60% stocks and shares (equity) split.

The Vanguard Target Retirement 2055 Fund has a split of 21% bonds and 79% shares and it adjusts it towards bonds as you get older!

Those are the main different types of funds you can buy into with Vanguard and other providers. The simple answer is that Katie and I invest solely in passive stock index funds. Specifically we have most of our net-worth invested in the Vanguard Developed World Ex UK. Look out for an upcoming article that compares the FTSE Global All Cap Fund and the Developed World ex UK. I haven't written that one yet and I am interested to see if writing the article shifts our own investment strategy going forwards. Katie and I learn as much, maybe more, from writing these articles as you do from reading them! Which type of fund should I choose?

Katie and I wanted to make this as easy as possible for you so here is the two of us talking through the Vanguard website and showing you where to click and what each part means!

Choice 3: Which specific index fund are you going to choose?

You are nearly there! When you get down to this level of the decision-making tree you are so CLOSE to a decision, there are only 15 funds to choose from! Please remember to just push through and start investing! The critical bit to building the future you desire is to start!

Back in 2016 when Katie and I were investing our first large lump sum we agonised over this decision! The truth is you can never actually know which fund is going to perform the best before you invest. You can only know that with hindsight! So we need to do is make the best choice that we can at the time, start and then tweak on the journey. Watch this 5 minute video that shows you the different index funds on the Vanguard site and then read on for how Katie and I make our decisions on what to invest in.

The Vanguard UK site splits up the index funds by location. You will see the global funds at the top of the list. Then as you scroll down you will see Europe, USA, UK, emerging markets and more. All we really need to do is decide which markets we want to invest in and how diversified we want to be.

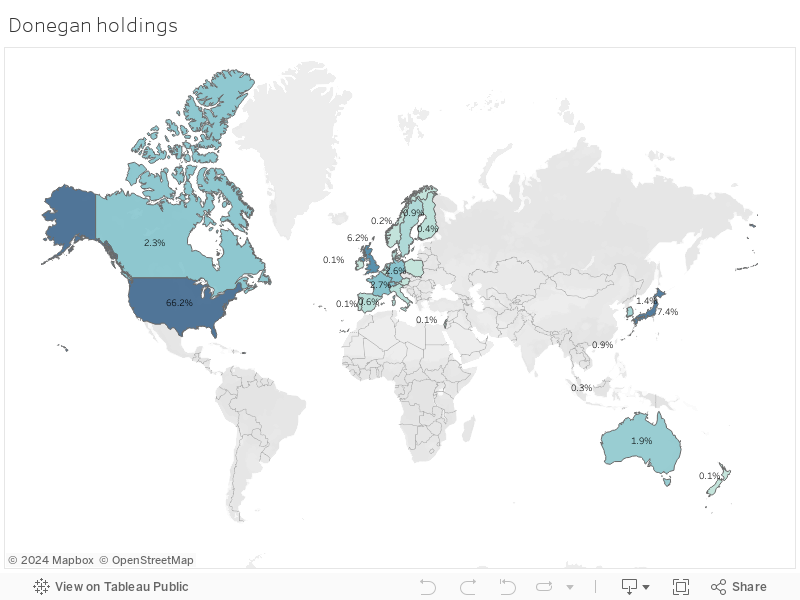

If you haven’t read the article on what is diversification yet then please go and read that first! If you want more on what an Index Fund actually is then read the second article in this series. Katie and I want to be globally diversified across all different sectors and companies. Our strategy is to own the entire world market. Jack Bogle the founder said it best when he said "stop searching for a needle in a haystack and just buy the haystack!" What he is referring to is people's search to find the next Google, Amazon or Airbnb that is going to grow dramatically. Just buy all the companies! When I first started index investing I choose the USA, the UK and the emerging markets. As we have learnt more about investing I wanted to diversify to the entire world. The question to ask yourself is how diversified do you want to be? Do you want to invest solely in the USA? The thing to remember here is that even if you invest solely in the USA you are already invested globally as most of the American businesses are global. Microsoft, Apple, Google and McDonald’s are already giant global businesses. So even buying just the USA index fund you are already investing globally. Katie and I are not American we are British (did you know that?). In investing there is something called home country bias. This is where you invest most of your money in your home country because that is what you know and understand! I can understand why people do this but it is a form of stock picking and therefore increases risk. I am not going to put all my money into British companies and hope they grow faster than the rest of the world and out perform everything else. I don't want to fall for home country bias. Katie and I don’t know which country is going to perform best in the future and we are not smart enough to be able to make good predictions. We therefore choose to buy a small percentage of every country's businesses around the world weighted to the size of their stock markets. The map below shows you where our finances are around the world.

Decision making criteria

The next article is going to show you how to read the individual fund pages on the Vanguard website and explain all of the different financial terms like risk profile, OCF and NAV price! It is incredible how similar it is to learning a new language at times!

The key to making a decision is to know the criteria you are using to make a decision and to know what is important to you as an investor. Here are the criteria that Katie and I use when decision making:

There are also some things that Vanguard puts front and centre on their website (as they should) that we don't think about at all when investing.

Global versus the developed world Ex UK

For people in the UK the two passive index funds that this normally boils down to are the FTSE global Index fund and the Developed World excluding the UK. Katie and I have been working hard to visualise the data for these two funds and to help you make a choice. We have a future article coming up that is going to analyse the differences between the two funds.

If you are in the USA then JL Collins invests in The Vanguard fund: VTSAX. I don't think you can go far wrong with this from an American perspective. From a European perspective I don't want all my eggs in the American basket. I want to be invested around the world To help you make a choice which specific index fund to invest in answer the following questions.

If you have made it this far you should be closing in on making a decision on which fund to go for! Before you press buy though............ SIPPS and ISAs / 401ks and Roths

It is important to think about using tax efficient vehicles for your savings and investments. What does this mean?

In each country you get to invest in tax advantaged accounts that the government creates to encourage you to save for your retirement. In the UK these are called Self-invested personal pension (SIPP), pensions or Individual Savings Accounts (ISAs). In the USA they are called things like 401Ks, IRAs and Roths. Taxation is an entire series of articles and there are lots of people that can help you to work out which ones you could use. I just wanted to highlight that you need to think about investing in tax advantaged accounts first and using your annual allowances! Do your homework! It is worth it. The Investor series and what's next!

Our next article will help you choose which index fund by looking at all the different information on the Vanguard website and breaking it down. We want to help you to be able to look at their website and feel confident clicking around and understand all the different terms.

Katie and I have been doing some filming so look out for the next article and video on that. The series of articles includes:

The purpose of these articles is to help you get going and take control of your finances. We are planning on running another Take Control of Your Finances Course in 2021 and will let you know when that is. In the mean time enjoy the articles and let us know how else we can help you in your goals and ideas. Remember you build your life. Start creating and building a life you can be proud of day by day. Your daily habits and actions build your life. It all starts there........ Alan Disclaimer

Neither Katie or I are trained financial advisors. This is just our opinion and sharing our thoughts with you. Please do your own research and make up your own minds on what to invest in.

Investments go up and down and if you haven't properly educated yourself and panic sell at the wrong time you could lose a fortune. DO NOT TAKE THIS STUFF LIGHTLY. Please learn, study and understand investing from the start! JL Collins - watch this......

As a complement to our investor series and course we can not recommend enough that you read JL Collins' book Simple Path to wealth and watch his Google talk . He is an incredibly good communicator and makes the complex easily understandable. Check out his google talk here:

|

RSS Feed

RSS Feed