BlogWelcome to the Donegans' blog. Start reading for help with investing, financial independence, lifestyle design, and many mini-experiments!

|

|

|

Back to Blog

4% Rule Questions - Retirement15/6/2021

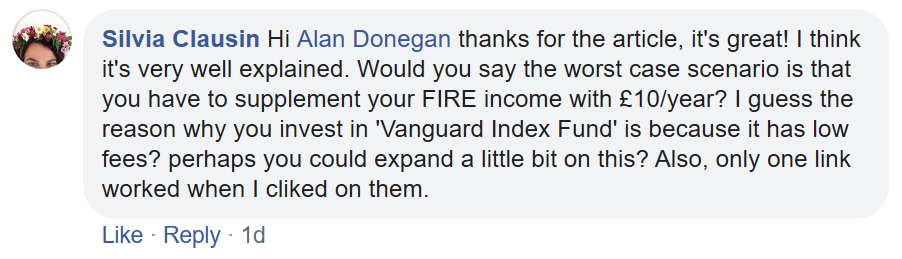

I originally wrote this on the 26th of May 2020 and updated it this week for you on 15th of June 2021. Has the advice changed following the pandemic? So here are all your questions about the 4% rule, early retirement and financial independence answered! Let's jump straight into "How much does it take to retire? The Q&A" with Alan...….. If you haven't read the original article on the 4% rule then start there as it clearly sets out the equations and maths behind knowing how much you need to retire! Can I get to financial independence with kids? Graham asks "Do kids knacker this?" The short answer is; No Kids do not knacker this but they do make it more challenging! I think what Graham is asking is do kids change the spreadsheet or the maths behind early retirement. The short answer is they don't change the maths but they do change the inputs. The 4% rule still stands and you still use it to work out the retirement pot you will need. This may be higher because of the kids but depends on if you want to retire before they are fully formed adults! The way to calculate the retirement pot you need is to take your annual expenses and multiply them by 25. According to research from the University of Loughborough the average couple spends £700 a month or £8375 a year to bring up one child for the first 18 years! This totals £150,753 spending in 18 years! That is going to change your inputs, i.e. the amount of money you spend each month. It doesn't change the basic equation which is expenses multiplied by 25. The basic maths says that if you need £8375 a year then you need a pot of £210,000 invested in broad based index funds to support that spending. If you are planning on retiring after your kids have grown up and you have stopped supporting them then your yearly spending "should" reduce so you will need less to retire on. Kids change the sums and it depends if you want to retire whilst still supporting your children or not? Bloggers such as Mr Money Mustache and Go Curry Cracker have kids and say that they don't have to increase expenditure that much! This is beyond my area of expertise though! In summary if you have children it will probably mean you have to earn more money in your life time to support them than a couple without kids. This will absolutely affect your retirement date but it doesn't change the 4% rule math at all. However if you are retiring after your children have flown the nest then you should calculate the amount of money you need based on your retirement spending levels which will reduce the size of the pot you need. Take the annual amount you want to live on in retirement (after they have flown the nest) and then multiply it by 25. This will give you the size of the retirement pot you should aim for! Having kids means you will probably spend more but it doesn't change the fundamental maths behind early retirement. The equations stay the same. What's the worst case scenario? Silvia has a few questions (plus I need to make sure my links work!) A lot of people do their retirement planning assuming they will NEVER earn any money ever again. So they tend to be more conservative in their planning. For me, if I get things slightly off and don't quite have enough for retirement then I can do 1 of two things:

I find there is always work and income if you go out positively into the world, so I have little fear of not being able to earn money in the future. Now I know this is different for different people so you may want to be a little bit more conservative than me. Worst Case Scenario: Earn more money to plug the gap or move to a lower expense country for a while. Silvia's second question is about the Vanguard index funds. Katie and I have chosen to put nearly all our investments into Vanguard index funds and this is for three reasons:

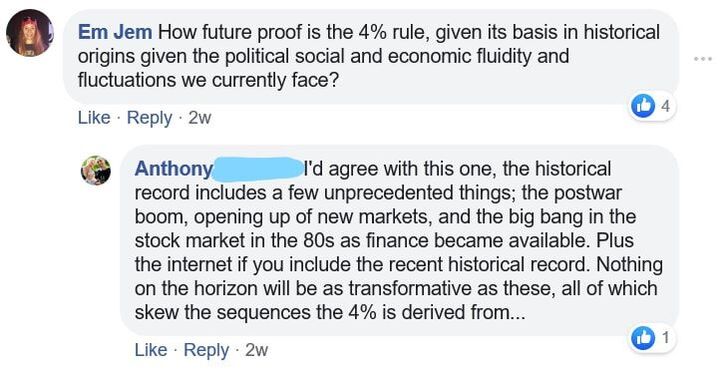

Low AMC fees on your index funds are critical when you are purchasing them. A index fund by definition tracks the index and will get average results so the main difference between providers is the company and the charges. Choose carefully between providers. How future proof is the 4% rule? How future proof is the 4% rule? My initial thoughts are:

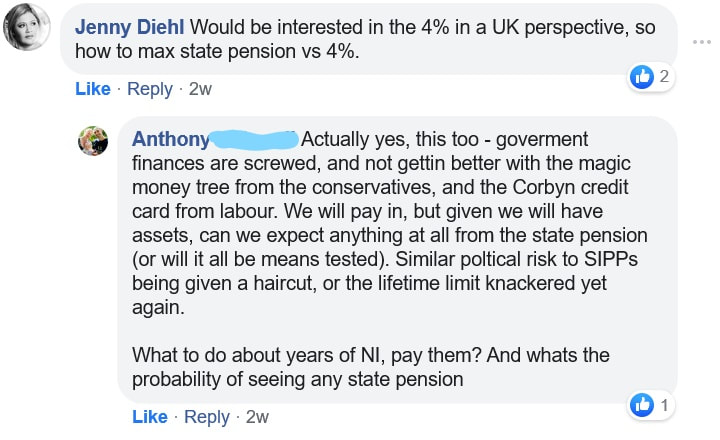

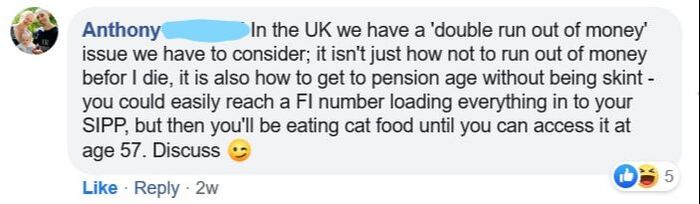

But does that mean we should write it off and just not use? Over the last 10 years VTSAX one of the Vanguard index funds has gone up by 13.42% on average. That is way above the 4% inflation adjusted you would be taking out. The maths supports a 4% withdrawal rate with a very high success rate! (this is pre-corona) I think the real question you are asking though is based in fear that the world is becoming more unstable and we face more political, social and economic uncertainty in the future than ever before. The second comment says the same and many people ask us given how bad things are getting in the world do we see it continuing like this! There will absolutely be problems and change coming which will require us to be flexible and do things differently. The market is going to crash again spectacularly, it is not if, it is when this will happen! The period the Trinity Study (this is what the 4% rule is based on) covered is from 1926 to 2011. This included World War 2, Vietnam War, 2 Iraq wars and so much more. As a world we have come through some unbelievable events and still survived. In many ways the world is in better shape than it has been before and is improving. Hans Rosling wrote a wonderful book called Factfulness that uses data to show how the world is improving. The media tells us the world is getting worse; which they do to get us to watch more; the world I see is very different to the one portrayed in the media. I found a 2 minute overview here by Bill Gates that is excellent! Do you think the world is improving or getting worse? Are you optimistic or pessemistic about our future? This is where it becomes difficult because no one can predict the future and it is up to each individual to decide whether they are going to be optimistic about the future or live in fear of what is going to happen next! I am very optimistic. I know the market will go up and down, I know there will be things that happen but I am positive that things will continue to improve. If world war three starts then we are all pretty screwed and none of this matters anyway. The second comment from above is from Anthony which seems to say that market returns are going to be lower in the future because we have invented everything already that has the power to transform our world. I disagree with this one. I think that the rate of invention, development and change is increasing and we are on the verge of some amazing new technology like artificial intelligence that is going to change the way we do things in the future. I think this is such an exciting time and I am pumped to see what happens next and what the world invents and creates. We have big data changing the way we look at things, artificial intelligence has the power to change everything, 3D printing changing the way we manufacture, blockchain technology could change finances, virtual reality and self-driving cars! There are incredible technologies coming that have the power to transform our world. This is going to create opportunities and change on a massive scale. I am an optimist and think things are going to keep improving. Can we predict the future? No! You have to decide if you are optimistic about the future or pessimistic about the future for yourself. I personally think the future is very bright and 4% is a conservative number. You will have to make up your own mind. There will always be a scare story available to make you think otherwise (that's how you sell newspapers and get people to watch the television!) Update: in October 2020 the guy who came up with the 4% rule wrote an article arguing that it should be higher; maybe even 5%. UK State pensions Jenny and Anthony discuss the state pension in the UK and will it still exist by the time we get there to claim it? I have a simple answer. I am NEVER going to rely on the government to look after me. I am going to look after myself. I don't trust the state pension will still be available when I retire. I am 41 years old and have 27 years until I can claim mine! The year will be 2046 and I have no idea how the British government is going to be doing or what will be happening in the world! If it is available then it will be a nice bonus. If not then I will not be relying on it. My plan is to base my finances on my own investments and I have not included any state pension in my figures at all. It is too far out to predict so I am choosing to look after my self and I will re-evaluate NI top ups as I get nearer the time. One last thought on the state pension is that most voters are older and it is in their best interests to keep the state pension going. Whilst I am not planning on it being there I am pretty sue that any government proposals to remove it are going to be faced with strong voting opposition! Will my money run out before I get to my pension? Anthony points out something that Katie and I have been considering and is actually the same the world over. If you invest money into retirement accounts that you can't access until a certain age then you need to make sure you have enough money available before that date. This one can be worked out with a fairly simple spreadsheet. I can not access my SIPP (Self-Invested Personal Pension) until 58 years old. So I have a gap from now (41 years old) of 17 years until I reach the age where I can access my pension. I need to make sure I have enough funds in other accounts to be able to cover me until then. Katie and I developed a spreadsheet that charted out our net-worth over the coming years. We projected out till we are 100 years old and how much our money would grow over the years. We marked when we could access the different accounts and worked to make sure we had enough funds in the accessible accounts that we could access before pension age. This is absolutely something you should consider and think about, but it is a fairly easy one to be able to chart in a spreadsheet and workout if you have enough to get through till traditional retirement! Should you adjust for assisted living/care home fees? Julia asks about assisted living and home care fees in old age. There are two ways I could take this question. Firstly it could mean caring for your parents as they get older. This can be a concern and it depends on a lot of factors. The country you live in, your parents financial situation and more. This is a complex question and I think the first step to think through is "will you be expected to provide for your parents in old age". This then leads to the question how much to you think you need to provide for them? If it is your parents you need to look after then I would be thinking about how much money I am going to have to earn to look after them. Secondly it could mean how much should you save for your own costs of old age and this again comes down to which country you live in and the style of old age you want to live. Some of the costs may be covered by government benefits and some might be born by the individuals. Assisted living in the UK currently costs between £500 - £1500 a week depending on the type. This is offset by the fact you wouldn't be paying rent or bills and have many other costs. It seems to me (and I am only 41 at the moment) that the money I have allocated for living on would shift to pay for the assisted living for myself and my wife when I come to it. For us being so far out this is going to become clearer as we get closer to the age and monitor our net worth and annual income. I think it is worth taking this into account as you plan how much you want to retire on. It doesn't affect the underlying 4% rule and how it works at all but as with kids it may raise the amount you need on a yearly basis and therefor the overall size of the pot you need. I think this is a personal decision based on how you want to live in the future. It's a guideline not a ruleThe 4% rule is a guideline not a rule. It is a guide and a simple equation that helps you to plan for the future. It helps you to make plans and is a basis for you to then question and expand your ideas and plans. You have to start somewhere. The simple place to start is the 4% rule. Take the amount you want to life off in retirement and multiply that by 25. This gives you the size of the pot you need to retire on. 4% is just the start. Then you need to dig into your own life, how you want to live, what you want to spend and your plans to be able to model out the finances and build the confidence you need to trust the plan. Thinking through the plan and the different nuances is so important to help you prepare for the future and an incredible and long retirement where you get to do whatever you want! What's nextMy first article on this subject was "What is Financial Independence" which was followed by "How much do I need to be able to retire?" which sparked all the questions for this article. I am sure there are going to be lots more questions and I have probably missed a few so please add yours below and I am planning a part 3 with more questions. I am also planning two more articles explaining how Katie and I have modelled out our finances and sharing an example spreadsheet and one about tax efficient savings in the UK. If you would like to stay up to date with the blog, FIRE (Financial Independence/ Retire Early) articles, startup thoughts and what is going on in the Donegan world then sign up to the mailing list below. Good luck with the financial planning and working towards a financially secure and free future! Love from Alan Disclaimer: This is not financial advice. Katie and I are not trained financial advisors, nor to we pretend to be one online. Read our full disclaimer here.

|

RSS Feed

RSS Feed