BlogWelcome to the Donegans' blog. Start reading for help with investing, financial independence, lifestyle design, and many mini-experiments!

|

|

|

Back to Blog

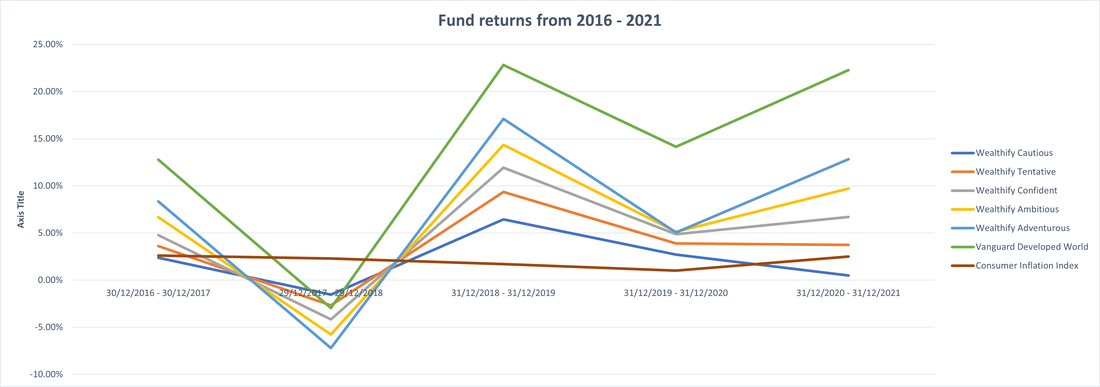

Wealthify review25/5/2022 Recently we were approaching investing and finance companies looking for sponsors for the Rebel Finance School to help us reach more people and do more good in the world. One of the companies we found was Wealthify and they seemed to have a great mission to simplify investing and help people make the most of their investments and pensions. On the surface it looked fabulous  We set up a call to speak to them and before we chatted we did a deep dive on their strategies and investment returns. Katie and I were SHOCKED with what we found. We wrote to Wealthify, cancelling the meeting. They asked for feedback, why did we cancel? We sent the feedback and their response was "we are going to have to agree to disagree." Wealthify has 30,000 customers and they are out there actively marketing (in my opinion unethically) for new customers. I decided to write an open letter to their CEO Andy Russell. If you have been thinking of investing with Wealthify read this first........ You are doing the opposite of making your customers wealthyDear Mr Russell, My wife and I did a deep dive into your investment strategies and performance of your funds and we didn't like what we found. This is an open letter to you to start the conversation about the performance of your funds and to see if we can get a better deal for your customers. I will happily post your response, if you have one, on my blog. I am happy to have my opinion changed if you come back with compelling data, I am happy to do a YouTube Live with you to discuss the investment strategy if you are open to it. You probably aren't going to like this open letter but I hope you take it as a opportunity to do better for your customers. This is the feedback I passed to your team. I am not sure if it made it through to you? So that you know where we are coming from…. we are big fans of simple, low-cost, passive index investing, like that provided by Vanguard. When we run the Rebel Finance School we talk about the two global passive index funds that Vanguard offers in the UK (the Developed world ex UK or the FTSE Global All Cap). Have you seen much of the research into index funds, Bogle heads, The Simple Path to Wealth and more? It’s interesting to read your factsheets and see that you are sort of “actively” investing in passive indexes. My understanding from the factsheets and your website is that you adjust which indexes make up each of the plans depending on market conditions. So you have turned passive investing into active investing. Active investors rarely if EVER beat passive index investing. Did you see the Warren Buffet bet? We looked at the returns on your funds over the last 5 years and compared it to the strategy of investing in a Vanguard global index fund (Developed world ex UK). Here’s what we found:

Data compiled as of: 24th February 2022 Here is a chart showing the returns over time. The top line is Vanguard's Developed world fund and everything below are Wealthify's funds showing consistent under performance. You seem to track the market roughly but just deliver 50% or more worse returns depending on the fund.  So even the most adventurous fund on Wealthify returns just over half what investing in a simpler Vanguard index fund (with much lower fees) returned over the last 5 years. If you had taken the money in the adventurous fund and passively invested that money instead in the Global Vanguard index fund, your customers would have got nearly DOUBLE the return. For every £10k invested in the adventurous plan, your customers would have been £4k-£5k worse off than in the Vanguard passive funds. And this is before fees have been taken into account. Your fees are 4 times higher than Vanguard's. I know you justify that by saying you are actively managing people's portfolios but your active management is damaging people's performance. Do you realise the impact fees have on people's long term finances? I like what you have done with simplifying the way of investing and trying to make it easier for people to get started, I just think you are doing them a disservice with these different risk tolerances. If people are in this for the long run (we are massive proponents of the buy and hold strategy), they should all just be investing in a global passive Vanguard index fund. Put it in the market and forget and about it and wake up wealthy decades later! I like that you try to be transparent and explain to people how the process works. The fund factsheets show a “typical investment” for each fund type. I know that’s because your fund managers are changing the makeup of each fund periodically. If I was invested in Wealthify I would want to know exactly where my money is. Looking at the factsheet for the adventurous fund, I’m curious as to why you have such a big home-country bias. 23% is invested in the UK which is significantly more than how much of the world the UK economy/stock market represents. What is the thinking here? Home country bias normally leads to under performing the market as a whole (apart from if you are from the USA since it accounts for such a big part of the global fund so the home country performance is highly correlated with the global performance) I know this is a lot of information. We have been in-depth researching index funds and investing for about 6 years now. Maybe it would be best to have a chat on the phone about this once you have had time to digest this! The promise of getting better than market returns or minimising losses through active management doesn’t ever play out. At first glance through your website we were super inspired by your transparency and use of simple index funds. Your cautious fund has barely kept up with inflation over the last five years. After 5 years of investing you have £20 in real terms to show for it. The company name, the marketing and the mission seem to be completely missing the mark. You aren't making your customers Wealthier you are making them poorer. Maybe you should change the company name to Poorify to more accurately reflect what you are doing? One last thing to mention. I think it is unethical that you put in your marketing materials that people get "an instant 25% tax relief top up". You make it sound as though this is what you get if you invest with you. EVERYONE in the UK gets this no matter who they invest with. You shouldn't need to sell this or bribe people with a prize draw for opening an investment account.

You are harming the financial future of your 30,000 customers and the people you are actively trying to persuade to invest with you. Alan Be careful who you chooseTo everyone reading this blog; investing is a mine field. Be VERY careful who you choose. Don't get bought in by flashy websites, awards or generous missions. CHECK the financials and the costs. Read the fine print and really understand what you are getting into.

Be careful. This is your financial future you are playing with. This letter uses lots of different financial terms. Sometimes learning finances can be a little bit like learning a new language. you need to translate it all! Here are some articles that relate to this letter that clear up some of the terms and impacts. |

RSS Feed

RSS Feed