BlogWelcome to the Donegans' blog. Start reading for help with investing, financial independence, lifestyle design, and many mini-experiments!

|

|

|

Back to Blog

This got me thinking, "Am I a risk taker?" What does the rest of the world see as risky that I see as the safe bet?

Do you think it is risky to start a business? Do you think it is risky to invest in the stock market? Do you think the safe thing to do is to get a job and stay there for the rest of your life? The definition of risk

Recently, Katie and I were running the Rebel Finance School and were talking about investing in low cost, broad based index funds (what is an index fund?). That is where we invest all of our money and we don't see it as a risky investment.

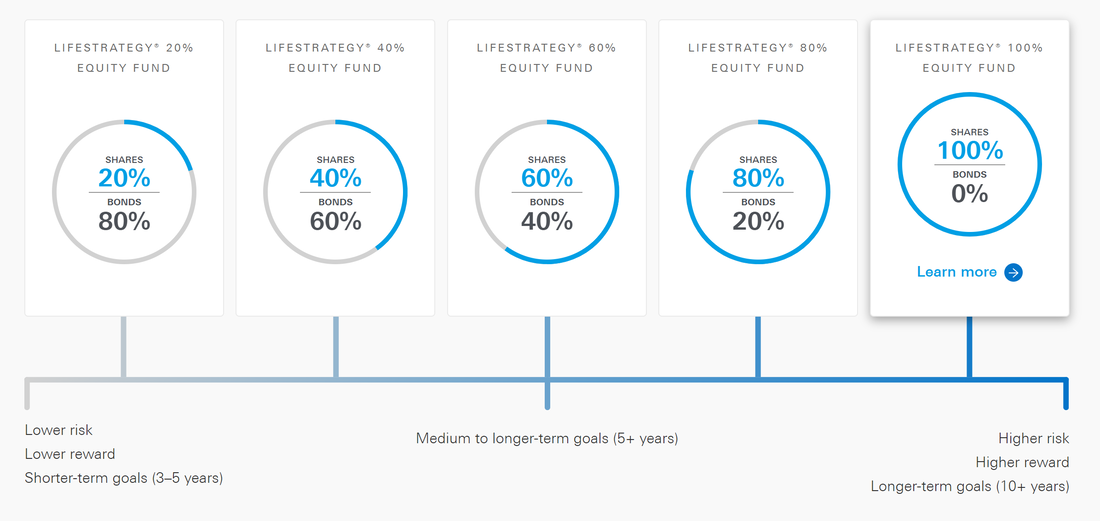

As we talked about our strategy and how we invest, one lady asked us what we would do in her situation. In the chat lots of people started commenting that we should ask her about her risk tolerance before we got to the strategy we would take. The investment strategy Katie and I follow is seen as one of the riskiest investments by financial institutions. We have 100% of our money invested in stocks and shares through index funds. SCARY!!! We don't have any bonds in our portfolio at all. Vanguard has a range of funds that they call Life Strategy funds. They are different mixes of bonds and stocks and shares. Here is how they show them on their website. On the left of the diagram is 80% bonds and 20% shares (the most risk averse) to the right-hand side at 100% stocks and shares (what they class as the riskiest)

I found this fascinating as I actually see this as the complete opposite to Vanguard. I think it's riskier to have more bonds in your portfolio. The reason I see it differently is because the higher percentage of bonds you own in retirement, the more likely you are to run out of money in retirement according to the Trinity Study (this is where the 4% guideline came from).

The higher the percentage of stocks and shares you have, the more likely you are to have money left at the end of your retirement. This is the exact opposite of the diagram I showed you above where they say more stocks and shares equals more risk. I started to wonder "How are they measuring risk?" How do you define risk?

Each Vanguard index fund has a risk score out of 7. The fund Katie and I are invested in is a 5 out of 7. Pretty risky on the scale.

I don't think it is risky at all though; so I started to wonder how they measure risk. Here is what I found in the help section: "This is the fund's synthetic risk and reward indicator (SRRI), an industry standard measure from 1 to 7" Well I don't know about you but that cleared it up for me! lol. What the heck are they on about? So I delved deeper to find out what the SRRI indicator actually is and this is what I found: In the European Securities Regulator's methodology document showing how to calculate the SRRI number of a fund they say: The synthetic risk and reward indicator shall be based on the volatility of the fund. So the European regulatory body is defining risk as volatility. This confused me a lot as volatility means the fund goes up and down a lot it but it doesn't equal your chance of losing money over the long term. Volatility and risk are two different things for me. My definition of risk is: "What's my chance of losing money?" I think it is risky if there is a high chance of me losing money and not very risky if there is a low chance of losing money. The EU governing body seems to think differently! Which makes it seriously confusing for investors and anyone trying to understand what to do with savings! Volatility versus risk

Our strategy is SUPER volatile but is it really risky?

The stock market is VERY volatile. This means it goes up and down a lot! When Covid hit, the stock market crashed because future earnings were in doubt, the economy was shutting down and things had gone cray-cray! Between 12th February 2020 and 23rd March 2020, the Dow Jones lost 37% of its value! That is HUGE. Katie and I had £186,000 knocked off our net-worth! That is huge volatility. This was only a paper loss as we never sold. The market bounced back; it always does over the long term. So where is the risk if you are investing for the long term? In the next year the stock market not only recovered but went on to set new highs that surpassed those of before. The stock market is always going up and down. It will crash again and it will surge again. We know there is another crash coming; there is ALWAYS another crash coming. So the stock market is volatile but does that mean it is risky? If you were to invest in a broad-based index fund that tracked the S&P 500 stock market, here are your chances of losing money over time, based on historical data:

If you invest for just a year then you have a 1 in 3 chance the stock market will be down at the end of the year. That is pretty risky for me. I have a low tolerance for losing money. However, if you invest for the long term (20 years plus), there has NEVER been a time in history that the stock market has ended up down. NEVER! So where is the risk if you are investing for the long term? The stock market is going to go up and down, it is going to surge and crash (volatility) but in the long term it always goes up (low risk of losing money) if you are invested in a broad-based index fund. Starting your own business without debt might be a rollercoaster of a journey (volatility) but if you started without debt, without borrowing where is the risk? Cautious funds versus risky funds

James (head of partnerships at Rebel), Katie and I have been looking for a sponsor to make Rebel Finance School sustainable. We would use the money to pay for web hosting, video hosting, content creation, promotion and a team to actually manage the events.

In doing so we have started to talk to some of the biggest players in the UK pension industry and having gone through their offerings in depth I am shocked at what they are offering customers and how they are pitching it.

Katie did vote years ago when we didn't know what we were doing in investing and her first ever stocks investment was into a cautious fund. Katie actively says she is risk averse and this fund seemed to match her level of adventurousness! What Katie didn't realise was that because she said she was low risk, her financial advisor put her in two funds, both of which only had about 45% in stocks and shares. This was when Katie was in her late 20s and she had decades of time to invest!

The financial advisor took risk to mean volatility not risk of losing money. With some reason. The companies think that if you say you are risk adverse then you will panic if your investments go down and sell them at the wrong time. Instead of educating you on the difference between risk and volatility they slap you in a cautious fund and damage your long term financial future.

Cautious funds in general get the worst returns over time. This is because they invest in underperforming assets such as bonds, cash and "safe / less risky options".

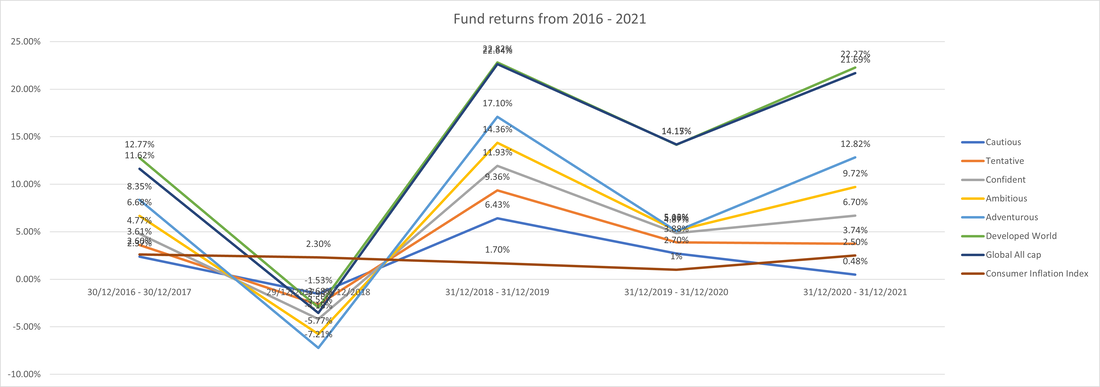

Advisors at investments firms around the world are conducting surveys asking if you are a risk taker or not. If they did a survey for me they would probably put me into the cautious fund too as I don't see myself as a risk taker. If they ever looked at what I was actually invested in they would see me as a huge risk taker. I see this completely opposite. For me the riskiest fund for you to be in for your financial future is the cautious fund. That fund doesn't even perform as well as inflation most years and your money is losing value every single year! WTAF. The fund they say is cautious is the one that you lose money in consistently?? I think the riskiest thing you can do for you retirement is put your money in the cautious fund. I know you love data like we do so let's get geeky baby. We took the above funds and then compared them to our two favourite funds, Vanguard FTSE Global All Cap and the Vanguard FTSE Developed World ex. UK, to see how they performed over the last five years. You can probably guess by now which fund returned the worst? Yes you are right! The cautious fund performed by far and away worst out of the funds we analysed. If you had invested £10,000 it would have grown over the last five years to a staggering £11,071! WOOOOHHHOOOOO Just keep up with inflation (i.e. your £10,000 has the same purchasing power 5 years later) you would have to have made £11,051. The cautious fund made £20 over inflation in the 5 years and that would have been easily consumed by fees, which we haven't even factored in here. If you had invested in the cautious fund you would have lost money in real terms. I find this crazy. I am paying a team of fund managers to lose money for me over the long term. Talk about risk! If you invest in this kind of fund you have a damn good chance of losing money over the long term. The other funds they had didn't do much better! Time for a chart of returns! The things I would love you to notice are that all the returns of the different funds pretty much chart the same course each year. You can see all the returns dipped in 2016 and then bounced back up the next year. The top two lines are the Vanguard passive index funds. The five funds below are the actively managed funds which have consistency under-performed the market. You have paid them extra, they have worked harder and they have got you FAR worse results. The bottom line on the chart shows inflation rates each year.

The top performing fund they had was the adventurous fund (designed for the risk takers out there!) This fund delivered an annualised return of 6.9% which is roughly half of what you would have got if you had bought the FTSE Developed world index fund at 13.4% return.

I think the finance industry has got risk back to front. The most risky thing you can do is give your money to trusted competent fund managers who will take time getting to know you and then actively trade with the promise of getting you better returns. In reality you get worse returns and pay higher fees for the privilege. The thing that the financial industry says is the most risky gets far better returns over time. £10,000 in this cautious fund over the last 5 years would have given you £11,071; the same £10,000 invested in the FTSE Developed World would have given you £18,759. That is £7,688 better off. Sometimes the "safest" thing you can do is the riskiest. It is all down to how you look at things and measure risk. I recently wrote an open letter to the CEO of Wealthify calling him out on his investment strategy. I have yet to get a response. Let's look at risk in a couple of different contexts Is it risky to start a business?

It is if you are borrowing a lot of money!

For years people have come up to me after the Rebel Business School courses that I run and said things like, "It's fine for you Alan, you're comfortable with risk!" I always look amazed as they say this especially after sitting through a 2 week course on starting a business without debt! Upon reflection it can be risky starting a business but that risk doesn't have to be money. You are probably going to have to risk time, energy and rejection but you don't have to risk money!

If you follow a more traditional approach to starting up I can see how that would be risky. You spend months writing a business plan and researching the market, you go and get investment or a loan to finance your business and go hundreds of thousands into debt, you create everything, make it perfect and then offer it to market. You hope that people will buy!

This way of doing this is HUGELY risky and I would NEVER want to do it this way. If you start this way you risk losing the money. One thing I do know is that if you do start your own business you are in for a volatile ride. Some days you will be on top of the world making sales and laughing and the next something will have happened to take the rug out from under you. You will be in for a rollercoaster journey but if you start without putting money in where is the risk of losing money? Is it risky to invest in the stock market?

The answer to this depends on how you are doing it!

If you are betting on different individual stocks, trying to time the market and dancing in and out then it is hugely risky. It is gambling. If you are investing for 15+ years in a broad-based index fund (What is an index fund?) then there is historically a lot of volatility but very little risk of losing money. Does this mean there will be no risk going forward? No, but it does mean it is one of the safer bets you can make. Katie and I feel so confident in this particular decision we have invested 76% of our net-worth into index funds and we are trying to sell off our rental properties and put the rest in too. Is Alan a risk taker?

Most of the world thinks so. Except Alan! lol

People look at me and think:

And in a way I am a risk taker but I don't risk my money. I will risk my energy, my time and my effort. I will put myself out there and build things and see if anyone wants them, but money? Money, my future, my investments? Those I will not risk. I am not going to risk the investments and money Katie and I have spend years building up. Not after watching my dad secure £3.6m ($5m) debt against the family home in the '90s and then lose all of it. Not after having to spend 10 years plus of my life fighting the banks and helping my mum try and keep a roof over our head. There is NO way I am ever doing something like that. I don't see risking my time as a risk that is going to be catastrophic. I don't see the risk of rejection as something that is going to cause me to lose my home and force me to fight the bank for a decade. I don't see risking my energy as a massive risk. I don't really see myself as a risk taker. I have taken a safe bet investing in index funds over the long term and I minimise any downside of entrepreneurship by starting my businesses without debt and for free. Why am I telling you this? Because I feel as though people look at me and think I am a risk taker and therefore OF COURSE I am going to say that investing in the stock market isn't risky. This just isn't true. After the family experience I have been through I hate financial risk and avoid it at all costs. Are you a risk taker?

The investment world LOVES to give us these little tests to check our risk tolerance. I think they are the biggest load of rubbish ever.

If you really understood the different ways to invest in the stock market you wouldn't see all of them as risky. If you saw the alternative ways to build a business with no debt you wouldn't see it as risky. If you really understood how often people get made redundant, restructured or forced to re-apply for their own jobs would you see getting a job as safe? For fun, I took one of the risk tolerance tests. I found the University of Missouri's risk tolerance test and took it to see how they would rate me!

My biggest bet......

To me, buying a broad-based global index fund and holding it over the decades feels like one of the safest bets you can make! I wouldn't have put my entire net-worth there if I didn't truly believe that.

Let me know what you think

As always Katie and I spend a huge amount of time writing these articles and we do it for you! We want to know what you think. Please take a second to like the post, leave us a comment, question or thought. It means the world to us.

Disclaimer: This is not financial advice. Katie and I are not trained financial advisors, nor to we pretend to be one online. Read our full disclaimer here.

|

RSS Feed

RSS Feed